How close is your state to committing Californiacide? Kevin Drum has your chart of the day.

Showing posts with label worst financial crisis since World War II. Show all posts

Showing posts with label worst financial crisis since World War II. Show all posts

Monday, November 16, 2009

Friday, November 06, 2009

The news from the economy remains pretty grim.

Sunday, April 26, 2009

Iceland after the crash.

Friday, April 03, 2009

Does the word postcapitalism look odd to you? It should, because you hardly ever see it. We have a blank spot in our vision of the future. Perhaps we think that history has somehow gone away. In fact, history is with us now more than ever, because we are at a crux in the human story. Choosing not to study a successor system to capitalism is an example of another kind of denial, an ostrich failure on the part of the field of economics and of business schools, I think, but it’s really all of us together, a social aporia or fear. We have persistently ignored and devalued the future—as if our actions are not creating that future for our children, as if things never change. But everything evolves. With a catastrophe bearing down on us, we need to evolve at nearly revolutionary speed. So some study of what could improve and replace our society’s current structure and systems is in order. If we don’t take such steps, the consequences will be intolerable. On the other hand, successfully dealing with this situation could lead to a sustainable civilization that would be truly exciting in its human potential.What comes after capitalism? Kim Stanley Robinson has a report on the future, while David Harvey investigates what comes right before what comes after capitalism.

Wednesday, March 18, 2009

Who could have predicted that putting the people who caused the problem in charge of fixing the problem would go so wrong? Say goodnight, Timothy.

Meanwhile, the situation at AIG may be much, much worse than anyone is admitting, while Kos and Josh Marshall are making sense: the real issues remain immediate triage of the economy, long-term systemic reform, and criminal prosecution of the widespread malfeasance throughout the financial sector. The bonuses suck, but they're really secondary. Let's not lose focus.

Saturday, March 14, 2009

27 Ways of Looking at the Financial Crisis. At FlowingData.

Wednesday, March 11, 2009

Time for a quick linkdump.

* Even Lex Luthor needs a bailout.

* Two for fans of last night's comics archetype times table: A Sketch Towards a Taxonomy of Meta-Desserts and Fun to Draw.

* Is this the end of capitalism? David Harvey and The Nation's Alexander Cockburn report. (This time for sure.)

Tuesday, March 03, 2009

For those who aren't already regular radio or podcast listeners, it's worth noting that this week's This American Life is another good show on the economy and the banking crisis. Until the next episode goes up over the weekend you can download this one for free; the previous two installments, The Giant Pool of Money and Another Frightening Show on the Economy, you've got to pay for you can stream for free but have to pay to download. (Thanks, Eric!)

Friday, February 13, 2009

A few more.

A few more.

* Wikipedia is doomed. Doomed!

* Storage closets of the American Museum of Natural History. With awesome slideshow, via MeFi.

* Tim Morton makes the simple but necessary point that as the only sentient agents in the area—the only beings with "response ability"—we are "responsible" for climate change whether we are "causing" it or not.

* Biggest solar deal ever announced. The article goes on to say "When fully operational, the companies say the facility will provide enough electricity to power 845,000 homes — more than exist in San Francisco — though estimates like that are notoriously squirrely."

* Washington Monthly tries to suss out Judd Gregg's erratic behavior.

* Legalize it? The real question is why haven't we yet.

* And Krugman (via Ezra Klein) says we may just be screwed.

And I don’t know about you, but I’ve got a sick feeling in the pit of my stomach — a feeling that America just isn’t rising to the greatest economic challenge in 70 years. The best may not lack all conviction, but they seem alarmingly willing to settle for half-measures. And the worst are, as ever, full of passionate intensity, oblivious to the grotesque failure of their doctrine in practice.

Tuesday, February 10, 2009

A couple of people have asked questions like Jon's about yesterday's chart of the day. Here's another version of the chart that's adjusted for population size:

By this measure it's the worst recession since at least 1981, with all but '58 and '81 having started recovery by now. More of these at FlowingData. Our economy's in bad, bad shape.

Monday, January 05, 2009

How does this happen? How can the person in charge of assessing Wall Street firms not have the tools to understand them? Is the S.E.C. that inept? Perhaps, but the problem inside the commission is far worse — because inept people can be replaced. The problem is systemic. The new director of risk assessment was no more likely to grasp the risk of Bernard Madoff than the old director of risk assessment because the new guy’s thoughts and beliefs were guided by the same incentives: the need to curry favor with the politically influential and the desire to keep sweet the Wall Street elite.The end of the financial world as we know it, in the New York Times. Widely linked this morning, but I first saw it on MetaFilter.

And here’s the most incredible thing of all: 18 months into the most spectacular man-made financial calamity in modern experience, nothing has been done to change that, or any of the other bad incentives that led us here in the first place.

Sunday, November 23, 2008

This thread from YayHooray (via MeFi) is easily the coolest thing I've linked to this year and possibly the coolest thing I've linked to in the entire time I've been doing this, with all the great flowcharts and infographics you've come to love from years on the innertubes. Some highlights:

This thread from YayHooray (via MeFi) is easily the coolest thing I've linked to this year and possibly the coolest thing I've linked to in the entire time I've been doing this, with all the great flowcharts and infographics you've come to love from years on the innertubes. Some highlights:

this week's blog icon, the LEGO anatomy chart

probably next week's blog icon, the gummi anatomy chart

the week after that, sci-fi awesomeness

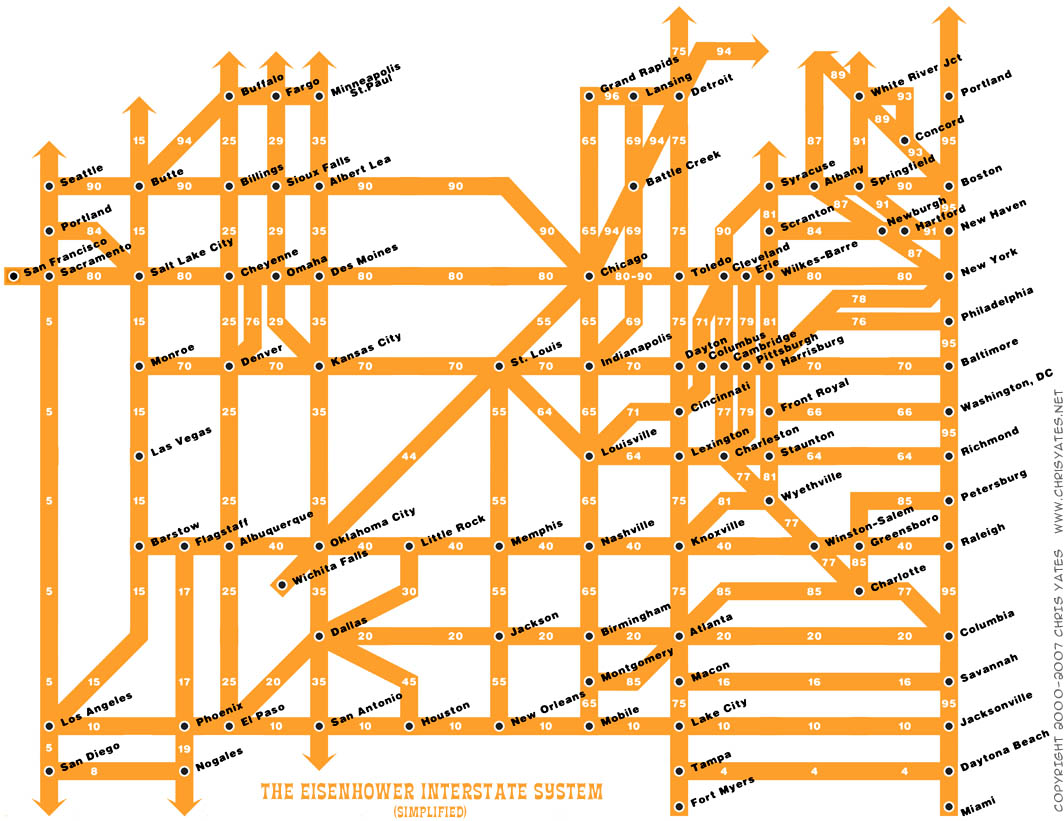

the interstate highway system as a subway map

your digestive system as a subway map

area codes in which Ludacris claims to have hoes

Sarah Palin pregnancy decision map

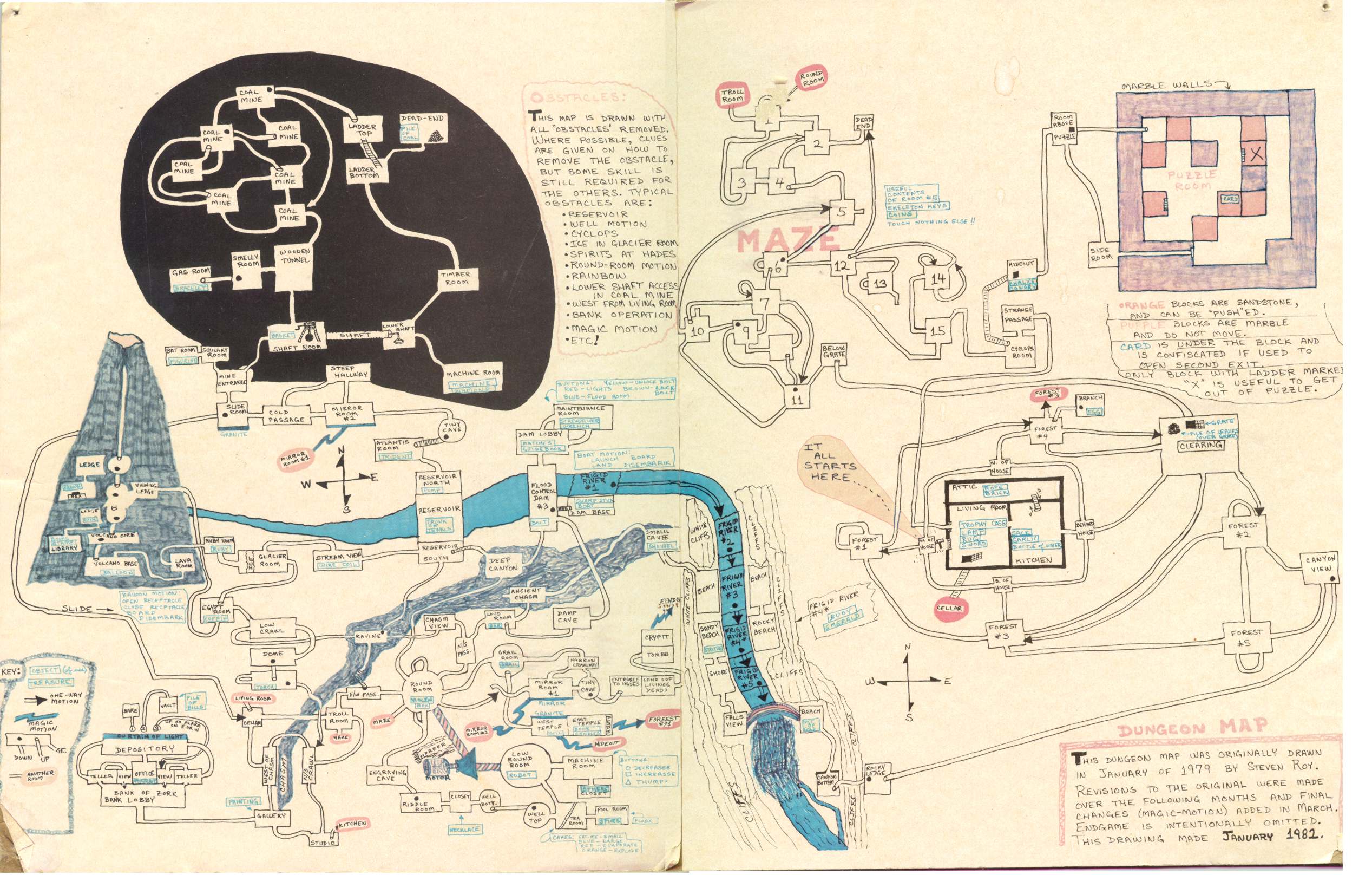

the map of Zork that doubles as my desktop

New Jersey invites you to come and see it all

extinction timeline, 1950-2050 narrative map of classic Choose Your Own Adventure novel The Cave of Time

narrative map of classic Choose Your Own Adventure novel The Cave of Time

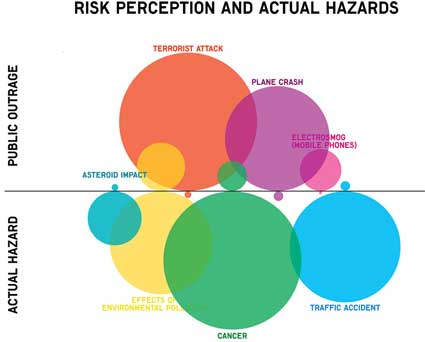

risk perception and actual hazards

a chart of how Americans spend their money that seems to strongly argue for a national salary cap around $100,000

a map of the United States expressed in terms of proximate distance from Knoxville, TN

the Indo-European family tree (and again)

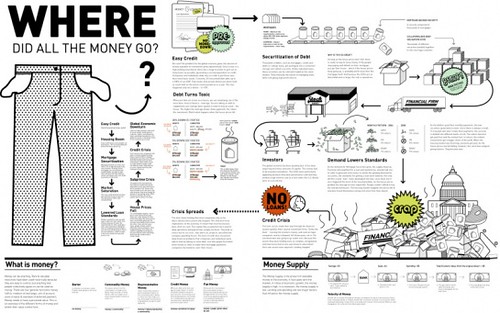

a visual guide to the financial crisis

a flowchart history of Cubism

Keep in mind those are just highlights. This is can't miss.

Wednesday, October 29, 2008

The end of libertarianism? "The financial collapse proves that its ideology makes no sense."

I could have told you that before the financial collapse.

Thursday, September 25, 2008

Jeffrey Toobin calls bullshit on the "suspension" of John McCain's campaign.

TPM also has word that McCain's ads will begin airing again on Saturday, deal or no deal—proving once and for all that this has been nothing more than a silly stunt, the only likely consequence of which is to scuttle a sorely-needed compromise on some sort of bailout.

Bloggers, who tend to consider themselves experts on everything, have by and large talked themselves into a completely incorrect position on this. I'm by no means an expert on the economy, either, but at least I understand the basic principle: the economy is an engine and the credit market is the oil. Run your engine without any oil and the thing will seize up.

This is not a joke, a scam, or a Bush Administration lie. What we're seeing in the markets is the real consequence of an environment in which banks are afraid to loan anyone, including each other, any money. Washington Mutual failed tonight—by far the largest bank failure in American history. This is a serious crisis. It may not require $700B+, and it certainly won't require the no-rules giveaway that Paulson favors, but it's going to take massive government intervention to keep the credit market afloat, and time genuinely is running out.

Luckily for me, I've never had a real job, so my non-existent 401(k) will be just fine. But if the economy seizes and the stock market tanks, and the country slides into the sort of severe economic downturn that the experts are warning us about, a lot of people will be broke and a lot more will be out of work—and you'll know exactly who's to blame for it.

Sunday, September 14, 2008

Monday, March 17, 2008

A brief history of the liquidity crisis, in cartoon form.

Via Matt Yglesias and everywhere else, this is why I'm glad I have no money:

Via Matt Yglesias and everywhere else, this is why I'm glad I have no money:

It’s just been announced that JP Morgan will buy Bear Stearns for $2 a share, implying a value of about $250 million. Given that the company headquarters is said to be worth about $1.2 billion, that gives the BS banking business a value of negative $1 billion. And that’s only after the Fed agreed to take on $30 billion worth of toxic waste from the BS portfolio, politely described as “less-liquid assets.”Bear Stearns, Wall Street's fifth-biggest investment bank, had opened at $60 a share on Thursday.

There's much more at Huffington Post, MetaFilter, and elsewhere, including Alan Greenspan's claim that this is the worst financial crisis since World War II. And he should know, he helped cause it.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}